We explore how large investors are changing environmental practises of companies from within…

When implementing a sustainable investment strategy there are multiple paths to take:

- ‘Screening’ is one of the most commonly used approaches, with the vast majority of asset managers claiming to be doing this across their investment universe. This consists of the exclusion of investments from a portfolio of the obvious bad stuff – fossil fuels, traditional sin stocks (tobacco, alcohol, gambling) and anything related to warfare or weapon production. That is, indicating the need for change from outside of the investable company.

Voting with financial feet is important. By divesting from certain industries, the business will be forced to pivot to retain their shareholders, or to attract new ones. That said, divesting a large holding isn’t realistic for large institutional investors who control around 70% of stock holdings in the U.S.- these firms are too large to move in and out of stocks with dynamism.

- So, the approach many of these investors take is ‘active ownership’ – that is, remaining invested in a company which is making all the right noises to become more sustainable, but holding them to account. Even applying some conditionality to the maintenance of that shareholding and guiding them through the process – all adds up to sustainable change from inside the investable organisation.

So how does active ownership work in practice?

Voting: when you buy shares in an organisation, you are usually issued with ‘voting rights’ – this means that you have a say in the running of that business. This, when you’re a large institutional investor, means your opinion can hold significant sway.

Topics which are typically voted upon are the appointment and remuneration of Directors, the appointment of auditors, donations to charities and political organisations and whether to issue more shares or declare dividends. So, if there was a director who didn’t show support for sustainable practises, there could be a vote to remove them from the board. Even if the vote isn’t significant enough to change a resolution, the presence of some opposition could start causing enough concern for the company – which could be picked up on by other shareholders at future votes.

The voting decisions of such investors are under increasing scrutiny with US firms, with independent industry ratings going some way to improve transparency as to where fund managers sit on the spectrum. Morningstar has recently published their findings, with some of the largest players, such as BlackRock, PIMCO and Vanguard being rated ‘basic’ or ‘low’ in terms of Environmental, Social and Governance (ESG) practices.

The brightened spotlight even caused Larry Fink, CEO of BlackRock to release an open letter, in an attempt to counter the public opinion of the firm’s lacklustre environmental voting record.

“ We will be increasingly disposed to vote against management and board directors when companies are not making sufficient progress on sustainability-related disclosures and the business practices and plans underlying them”

What is Stewardship?

A much more integrated approach which goes further than voting. Engagements are made by the investors with the company directors to drive the direction of travel for practises and future strategies where ESG issues may have arisen. Key shareholder groups have also historically teamed up in these practices to add more clout to the proposals they’re making.

“Stewardship is the responsible allocation, management and oversight of capital to create long-term value for clients and beneficiaries leading to sustainable benefits for the economy, the environment and society”

FRC, UK Stewardship Code, 2020

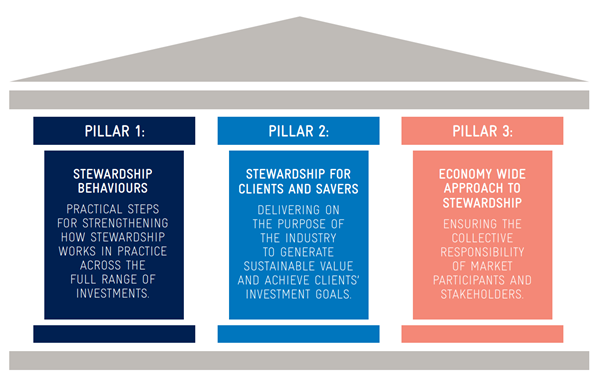

Taking this collaborative approach further, the UK’s Investment Association has formed a Stewardship Working Group which has outlined three necessary pillars to unify stewardship approaches: (per the below diagram)

• Stewardship in the UK Stewardship behaviours;

• Stewardship for clients and savers; and

• Economy wide approach to stewardship

Successful stewardship engagements

Stewardship is a long-term approach to improved ESG transparency and responsibility, and so followers and lobbyists are warned to be patient, but there is reason for hope, especially in the transparency practices of some of the world’s most controversial industries.

For example:

• Shell & Kempen investment managers

In December 2018, a joint statement between Shell and CA100+ investors (including Kempen), announced the steps the firm was taking to further align to the Paris Agreement. This included short-term targets and the linkage to remuneration, plus an assessment of their memberships with industry associations, all due to the concerns raised from its shareholders.

• Amazon and Bank of Montreal Global Asset Managers

BMO GAM held concerns around a lack of transparency with regard to the firm’s sustainability disclosures. They coordinated with other investors to co-file a resolution pushing for dialogue and exposure to ESG related issues.

“Over the last year we noticed Amazon’s attitude beginning to change, with two significant sustainability announcements – the Global Human Rights Principles and its ambitious goal to be net zero carbon by 2040. Our future engagement will be focusing on the implementation of both of these newly stated ambitions.”

Despite the additional pressures on the aviation sector as a result of the COVID 19 pandemic, Rolls Royce’s investor base, including the UK’s Hermes Fund Managers to continue to commit to playing a lead role in the sector’s aim to achieve net zero emissions by 2050.

The investor base defined the need for new interim targets, an advancement of its climate-related financial disclosure, to consider connecting director compensation to climate performance metrics and most pertinently, continuing R&D into low-carbon technologies.

Whilst stewardship has come a long way since the global financial crisis, it isn’t necessarily always the most positive approach for all investors – more short-term ‘activist shareholders’ can buy and then offload large chunks of organisations, which could leave smaller shareholders at the mercy of the resultant share price fluctuations.

Likewise, it has to be remembered that not all companies are open to working with its investor base, and so, may only engage at surface level to maintain appearances. As a relatively new approach, the longer term implications for both stewardship practises and their impacts is yet to be seen – yet it’s safe to say that greater transparency into the plans, albeit future ones, of some of the world’s largest companies can only be a good thing.

Be Curious

• Your pension pot will be run by a large investor – take a look and see if they are holding companies to account – do they have an ESG strategy you can switch to? Are they voting how you’d like regarding sustainability related resolutions?

Yes, the power in stewardship is with the large investors – but if there is enough demand from the individuals, the pressure will continue to reap green rewards.